Here’s a number that should make you sit up straight: the global supply chain control tower market for the oil and gas industry is expanding at a clip that suggests not just growth, but a fundamental retooling of how energy flows across the planet. North America, with its established IT backbone, currently leads the charge, but the real story—the one whispered in the data centers and command rooms from Houston to Dubai to Singapore—is the accelerating adoption in the Middle East and Asia-Pacific. Why? Geopolitical volatility and the ever-present specter of maritime supply chain risk are forcing a reckoning. And this isn’t a one-size-fits-all scenario; the very strength of control tower vendors fractures depending on whether you’re poking for oil deep underground, pushing it through miles of pipeline, or selling it at the pump.

The Segmented Battlefield: Who’s Who in Control?

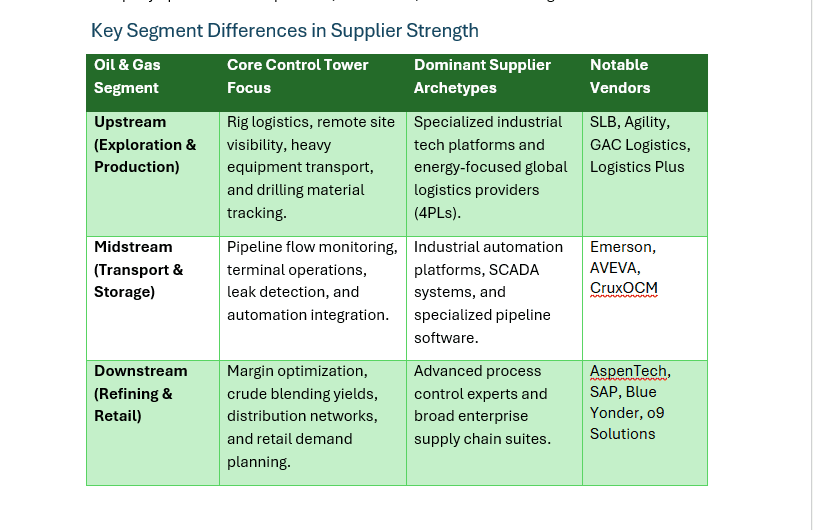

Forget a monolithic market. The oil and gas sector is a hydra, and its supply chain needs are as varied as its operational segments. Upstream, the exploration and production game, is all about getting heavy equipment to remote sites and tracking every drill bit. Here, you’ll find specialized industrial tech platforms and the big 4PLs (fourth-party logistics providers) that manage it all. Think SLB, Agility, GAC Logistics – the folks who make sure the gears turn in the most challenging environments.

Midstream, the artery of the energy world, focuses on pipeline flow, terminal ops, and—critically—leak detection. This segment leans heavily on industrial automation giants like Emerson and AVEVA, alongside specialized pipeline software wizards like CruxOCM. They’re the guardians of the flow, ensuring efficiency and safety.

Downstream, the refining and retail end, is where margins are squeezed and demand planning becomes king. This is the domain of advanced process control experts and the big enterprise suits. AspenTech, SAP, Blue Yonder, o9 Solutions—they’re all in the business of optimizing yields, blending crudes, and predicting what you’ll want to put in your car next Tuesday.

The Data Deluge and the Bullwhip Effect

The global market for these control towers is currently experiencing an almost frantic, explosive growth. It’s a cultural shift, no doubt. For decades, oil and gas operated on sheer brute force, massive scale, and siloed departments that rarely spoke the same digital language. Now? They’re being forced into a collaborative, data-driven ecosystem. These control tower platforms aren’t just fancy dashboards; they’re aggregating data from every conceivable source—ERP systems, remote pipeline sensors, even the ever-shifting sands of geopolitical news feeds—to create that elusive single source of truth. And the stakes are high. This digital agility is precisely what’s needed to combat the infamous “bullwhip effect.” You know, where a tiny tremor in global energy demand can send massive, inefficient tidal waves through production schedules and inventory levels. It’s chaos, tamed by data.

Why Does Control Tower Adoption Vary So Much by Region?

It’s not just about having the latest tech; it’s about what keeps you awake at night. Regional adoption of these control towers is painted by the brushstrokes of local priorities, the maturity of IT infrastructure, and, crucially, the immediate geopolitical risks. North America, with its strong IT and vast domestic production hubs like the Permian Basin, accounts for a hefty 37% of global control tower revenue. They’re orchestrating complex upstream logistics and optimizing LNG exports.

The Middle East, however, is playing a different game. Their focus is on resilience and energy security, driven by massive natural gas expansion. Companies like Saudi Aramco are plowing investment into control towers integrated with AI and blockchain, not just for operations, but to safeguard vital maritime transit routes. It’s about stability in a volatile neighborhood.

Asia-Pacific is the hotbed of rapid growth, largely due to its immense reliance on imported energy and the perilous transit routes involved. Think the Strait of Hormuz. For APAC energy firms, control towers are a lifeline for tracking inbound ships, managing terminals, and bracing for those sudden geopolitical supply shocks that could otherwise cripple their economies.

Europe, meanwhile, is a unique beast. Their adoption is intrinsically linked to stringent regulations and the global energy transition. Control towers there aren’t just about efficiency; they’re about tracking carbon footprints and ensuring ESG compliance. It’s efficiency with an ethical overlay.

Supplier Fragmentation: A Necessary Evil?

The oil and gas supply chain is inherently fragmented. Trying to shoehorn a universal control tower solution is like trying to fit a square peg into a round hole—it just doesn’t work. Supplier strengths are wildly divergent. The companies dominating upstream logistics are often not the same ones optimizing downstream refining. This fragmentation, while potentially challenging, also fosters specialization. Vendors are forced to hone their offerings for specific niches, leading to deeper expertise and, theoretically, better outcomes for their clients. It’s a complex ecosystem, but one that’s increasingly reliant on intelligent digital oversight.

Vendor Landscape by Segment

| Oil & Gas Segment | Core Control Tower Focus | Dominant Supplier Archetypes | Notable Vendors |

|---|---|---|---|

| Upstream (Exploration & Production) | Rig logistics, remote site visibility, heavy equipment transport, and drilling material tracking. | Specialized industrial tech platforms and energy-focused global logistics providers (4PLs). | SLB, Agility, GAC Logistics, Logistics Plus |

| Midstream (Transport & Storage) | Pipeline flow monitoring, terminal operations, leak detection, and automation integration. | Industrial automation platforms, SCADA systems, and specialized pipeline software. | Emerson, AVEVA, CruxOCM |

| Downstream (Refining & Retail) | Margin optimization, crude blending yields, distribution networks, and retail demand planning. | Advanced process control experts and broad enterprise supply chain suites. | AspenTech, SAP, Blue Yonder, o9 Solutions |

This granular approach underscores a critical point: the success of a control tower solution hinges on its ability to speak the language of its specific operational segment. Generic platforms will likely falter where deep, industry-specific intelligence is required.

The Future: Integrated and Intelligent

So, what’s next? We’re likely to see even tighter integration between these control towers and other critical operational technologies—think IoT sensors, advanced analytics, and even digital twins. The goal is clear: to move beyond mere visibility towards predictive and prescriptive capabilities. The oil and gas industry, often perceived as slow to adapt, is in the midst of a profound digital metamorphosis, driven by the undeniable necessity of strong, intelligent, and globally connected supply chains. The control tower is the conductor of this increasingly complex orchestra.