Can Amazon’s vast logistics network actually chip away at the duopoly of FedEx and UPS, or is this just another Amazonian overreach?

Amazon’s quiet-but-significant move to open its sprawling logistics network to outside businesses under the umbrella of Amazon Supply Chain Services (ASCS) presents a fascinating, and frankly, slightly terrifying, prospect for the established titans of transportation. This isn’t merely an extension of its existing seller services; it’s a full-throated embrace of third-party logistics (3PL) that could, over time, fundamentally reshape market dynamics. While experts don’t foresee an immediate collapse of FedEx or UPS—these are behemoths with deep roots and specialized services—Amazon’s relentless march into this space demands a sharp, data-driven eye.

The Unbundling of Amazon’s Might

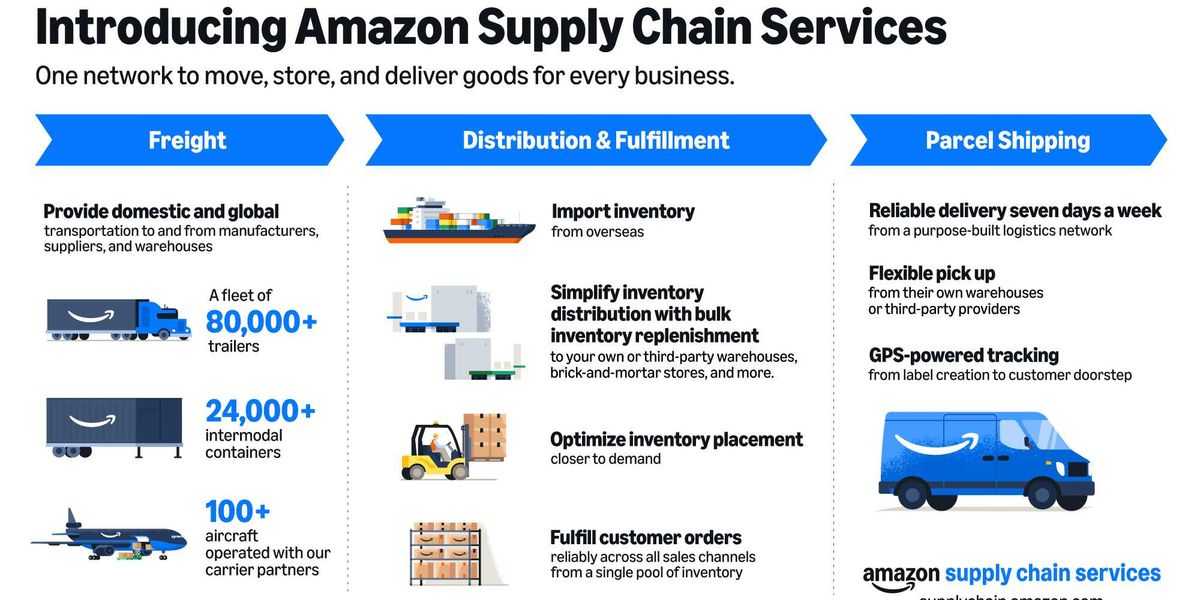

For years, Amazon has been quietly building what is, by all accounts, the most sophisticated and integrated logistics machine on the planet. They’ve mastered parcel delivery, built out a formidable trucking arm, and perfected fulfillment with a speed and scale that’s frankly astonishing. Now, they’re packaging it all up. ASCS isn’t just a concept; it’s a tangible offering combining freight transport, parcel shipping, and distribution, all powered by Amazon’s existing infrastructure—its warehouses, its trucks, its planes. This is a crucial distinction from its previous offerings, which were largely siloed or tied to sellers on Amazon. This new model opens the door to any business.

Matthew Hertz, CEO of Third Person, rightly points out this isn’t an overnight revolution. Amazon has been steadily gaining ground with services like Amazon Shipping and Multichannel Fulfillment. The real story here is organic growth. Hertz predicts Amazon will continue its market share creep over the next three years, a projection that aligns with Amazon’s historical modus operandi: build, scale, dominate, and then, if profitable, monetize beyond its core.

Parcel Pricing Pressures and Strategic Retreats

Nate Skiver, a parcel analyst at LPF Spend Management, hits the nail on the head regarding the parcel delivery segment. Amazon Shipping, offering a two-to-five-day window, is poised to create significant pricing pressure, particularly on smaller, price-sensitive carriers. These players often differentiate solely on cost; Amazon entering the fray with its scale and efficiency will force difficult choices. Skiver notes that even FedEx and UPS, while prioritizing higher-value niches like healthcare logistics—segments requiring more complexity and commanding better margins—are not immune. Their strategic shift away from lower-value residential e-commerce shipments, where Amazon excels, creates a void ASCS is perfectly positioned to fill.

This is where the human element of strategy really comes into play. FedEx and UPS, sensing the shifting sands and the relentless competition in pure e-commerce parcel volume, have wisely begun to pivot. They’re focusing on segments where Amazon might struggle to replicate the precision and specialized handling required. It’s a smart defensive move, but it also leaves them potentially vulnerable in the very areas where Amazon’s core competencies lie.

Trucking: A Different Battleground

The trucking side of ASCS presents a more nuanced challenge. Scooter Sayers, an LTL consultant, is quick to note that Amazon’s current capabilities in less-than-truckload (LTL) are, for now, geographically limited, primarily serving inbound shipments to Amazon facilities. To truly compete with LTL giants like FedEx Freight or Old Dominion, Amazon would need a massive expansion of its own infrastructure and driver network. This isn’t impossible, of course, but it’s a significantly higher barrier to entry than expanding its parcel network. The sheer volume and complexity of LTL operations require a different kind of animal—one that Amazon may still be grooming.

Fulfillment: The Unfamiliar Territory Made Familiar

Fulfillment, however, is Amazon’s bread and butter. Through Fulfillment by Amazon (FBA) and more recent offerings like Amazon Warehousing and Distribution, they’ve been doing this for third-party sellers for ages. Derek Lossing, founder of Cirrus Global Advisors and a former Amazon logistics leader, highlights this point starkly: Amazon already fulfills billions of parcels for external parties. The bundling of these services—transportation, distribution, fulfillment—under the ASCS banner is the key differentiator. It’s the cohesive package, marketed broadly, that elevates the competitive threat from an incremental one to a potential paradigm shift for businesses seeking a single-vendor solution.

Who’s Signing Up?

Don’t mistake this for vaporware. ASCS is already attracting major players. We’re talking 3M and Procter & Gamble for trucking; Lands’ End for inventory positioning; American Eagle Outfitters for parcel shipping. Avacraft, a cookware seller, use Amazon’s warehousing before ASCS was even a formal product. KiwiCo and Bark have used Amazon Shipping for speed and cost savings. This isn’t a niche play; it’s a broad appeal to businesses, especially fast-growing ones, that need a one-stop shop from manufacturing all the way to the end consumer. Lossing correctly identifies direct-to-consumer shippers and omnichannel retailers as prime targets, particularly those focused on lightweight residential volume.

The Caveats and the Lingering Questions

So, what’s the catch? Beyond the obvious competitive threat to FedEx and UPS, there are significant operational questions for ASCS customers. The most pressing, and one Amazon declined to comment on, is capacity allocation. How will Amazon prioritize its own marketplace inventory versus third-party ASCS clients, especially during peak seasons? We’ve seen Amazon advise sellers to get holiday inventory in early to avoid capacity crunches. Managing that internal capacity constraint is already a challenge; extending it to external clients could amplify these issues considerably. The current ASCS customers, while impressive, are likely early adopters. The real test will come when ASCS faces sustained demand and the inevitable operational hiccups that plague even the most efficient logistics networks.

This move by Amazon is less about immediately dethroning FedEx and UPS and more about a calculated expansion into a lucrative market where its operational DNA is already a near-perfect fit. It’s a strategic play for market share that traditional carriers cannot afford to ignore. The long-term impact hinges on Amazon’s ability to manage capacity, maintain service levels across a broader client base, and continue to innovate in an industry that, despite its traditional image, is in constant flux.

FAQ

What is Amazon Supply Chain Services (ASCS)?

ASCS is a suite of logistics services offered by Amazon to any business, encompassing freight transportation, parcel shipping, and distribution and fulfillment, utilizing Amazon’s extensive network of fulfillment centers, trailers, and aircraft.

Will ASCS immediately replace FedEx and UPS?

Experts do not believe ASCS will immediately eliminate FedEx and UPS. While it presents a significant competitive challenge, particularly on pricing for parcel delivery, established providers have diversified and prioritized higher-value logistics segments.

What are the main concerns for businesses using ASCS?

A primary concern is how Amazon will manage capacity allocation between its own marketplace inventory and third-party ASCS clients, especially during peak shipping seasons, and potential for compounded capacity constraints.